January 2019 Monthly Spending Report and Debt Update

Welcome to my first ever Monthly Spending Report and Debt Update! In this post, I’m going to be sharing a recap of my monthly income and expenses, so you can see exactly how my budget and debt pay-off went this month!

Before we get started, let me share a quick recap of how we budget in our house.

My husband and I keep our money separate.

To begin, my husband and I keep our money in separate checking accounts.

Gasp. I know. Yes, we’ve been married 7 years already, and yes, I know Dave Ramsey says to combine finances. But, honestly, I’m just not at that point yet. He’s a spender and I’m a saver, and I think combining finances—with two people spending from the same pile of money—sounds like a disaster to manage. If combining finances works for you, fantastic! It’s just not what we’ve chosen to do in our home.

My husband and I split the bills.

My husband and I split the bills. I take the mortgage, home owner’s association dues, and property taxes. He takes everything else (car insurance, utilities, and groceries, and cash flowing college for his 20 year-old son). This works for us.

I share my half of the budget.

Hubs isn’t completely on board with sharing 100% of our income and spending plans with complete and total strangers on the internet. Thus, the budget recaps you’ll see here are my portion of the budget only. But, I will share real honest numbers with you, so hopefully you’ll get a feel for how a real budget works and functions.

OK, with all that out of the way, let’s get started!

Income

My total income for January 2019 was $6,395.94, broken down as follows:

$5,531.61 from my regular paycheck from my regular job as a civil defense attorney.

$114.33 from affiliate marketing for a home decor blog I started in 2017 and have basically completed abandoned. (If you’re interested in finding out how to earn money with affiliate income—you don’t need a blog!—see this post!)

$750.00 donated from hubs’ pay, for the purpose of making extra debt payments.

Spending

Each month, I create a zero-based budget, allocating my income across all budget categories, until I’m left with 0. You can see my actual budget for January in my saved stories on Instagram.

Any additional money that comes in during the month (in this month’s case, $114.33 from affiliate marketing and $750 from hubs) goes straight to debt.

If you add everything up, you’ll notice that what I spent in January is actually higher than what I earned in January. This is because I paid for some of my expenses out of sinking funds that I have saved up over time (medical, for example), and were not completely covered with this month’s pay.

Here’s how I spent the money in January:

Mortgage - $1,770. We have a 30-year fixed rate mortgage (which I wish was a 15!). We ultimately plan to pay it off FAR sooner, once we tackle our non-mortgage debt and beef up our emergency fund.

Life Insurance - $49. I pay monthly for a 20-year level-term life insurance policy.

Cell Phone - $171. Yes, this is painful. And yes, it’s only one cell phone. I have AT&T and unlimited everything. Too nervous to make the switch to a budget cell phone provider, but maybe one day.

Student Loan - $3,612. This includes my $375.63 minimum payment plus $3,237 in extra payments. Our student loan is the only debt we have, and we have an ambitious goal of paying it off in 2019. A further breakdown of how I was able to pay $3,237 in extra payments is down below.

Gasoline - $161. Gasoline is higher than usual this month, because I had to drive for work from Houston to Dallas. Those costs will be reimbursed to me, however.

Tolls - $180. I have a 3-hour daily commute (an hour and a half each way—JUST to drive 25 miles in horrific Houston traffic). I happily pay extra to REDUCE my drive time down to ONLY three hours a day. This is ridiculous, I know. But, it’s the nature of the beast, and something I’ll gladly spend money on for now, even though it’s outrageously expensive.

Parking - $5. As an attorney, I often have hearings downtown at the courthouse, which require paid parking. I get reimbursed for these expenses, however.

Entertainment - $19. This figure is what we pay for Netflix/Hulu.

Kid Activities - $30. This month, the school sponsored a Mother Son Fun Night at a local funplex, complete with laser tag, bowling, and arcade games. I wasn’t about to pass it up.

Clothing - $37. At above-mentioned fun kids’ activity, I put my jacket down at a table, turned around, and then it was gone. I checked lost and found several times, and nothing. And, aspiring minimalist that I am, it’s the only jacket I have and wear. I seriously wear this thing everywhere. I was soooo disheartened that it was stolen. I mean, seriously, who does that? I typically do not buy clothes if I can help it (I have more than I need as-is), but I did need to replace my only jacket. I ordered a replacement through Ebates, and earned 3.5% cash back on the purchase. (If you sign up with my link, you’ll get a free $10 to spend, and I’ll also earn a referral bonus!).

Medical/Dental - $201. A doctor’s visit and a prescription.

Eating Out - $75. I set a goal not to spend any money eating out this month. But, my sister came into town for a couple of days, twice this month, and both times we hit up one of our favorite food trucks, and I treated her to lunch. (She can’t get Korean tacos in the small college town where she lives, and we’re both kinda obsessed with them). I also spent to buy my son a cake pop at Starbucks and a snack at Panera Bread during her visit. I also splurged on dinner at Chick Fil A for the whole family one night. Next month, I’ll set a higher figure for eating out, because I’m sure I’ll be able to stick to it better than having a $0 budget for eating out. Having nothing was a mistake, which caused me to dip into my buffer and my fun money for eating out. Live and learn.

Save As You Go - $21. I bank with Wells Fargo, and I’m enrolled in a program that takes $1 from your checking account every time you use your debit card and puts it in your savings account. It’s an easy way to automate savings and helps build your savings up, over time, and you barely notice.

Miscellaneous - $35. This included mainly household and grocery items like face wash, eye makeup remover, moisturizer, and a couple of boxes of cereal.

Subscriptions - $24. This is for Dropbox and Pic Monkey. I honestly thought I successfully cancelled Pic Monkey in December and was surprised to see the charge come through. I constantly use Dropbox for work, but at $127/year, it may be worth finding free alternatives or seeing if they will reimburse me for the cost.

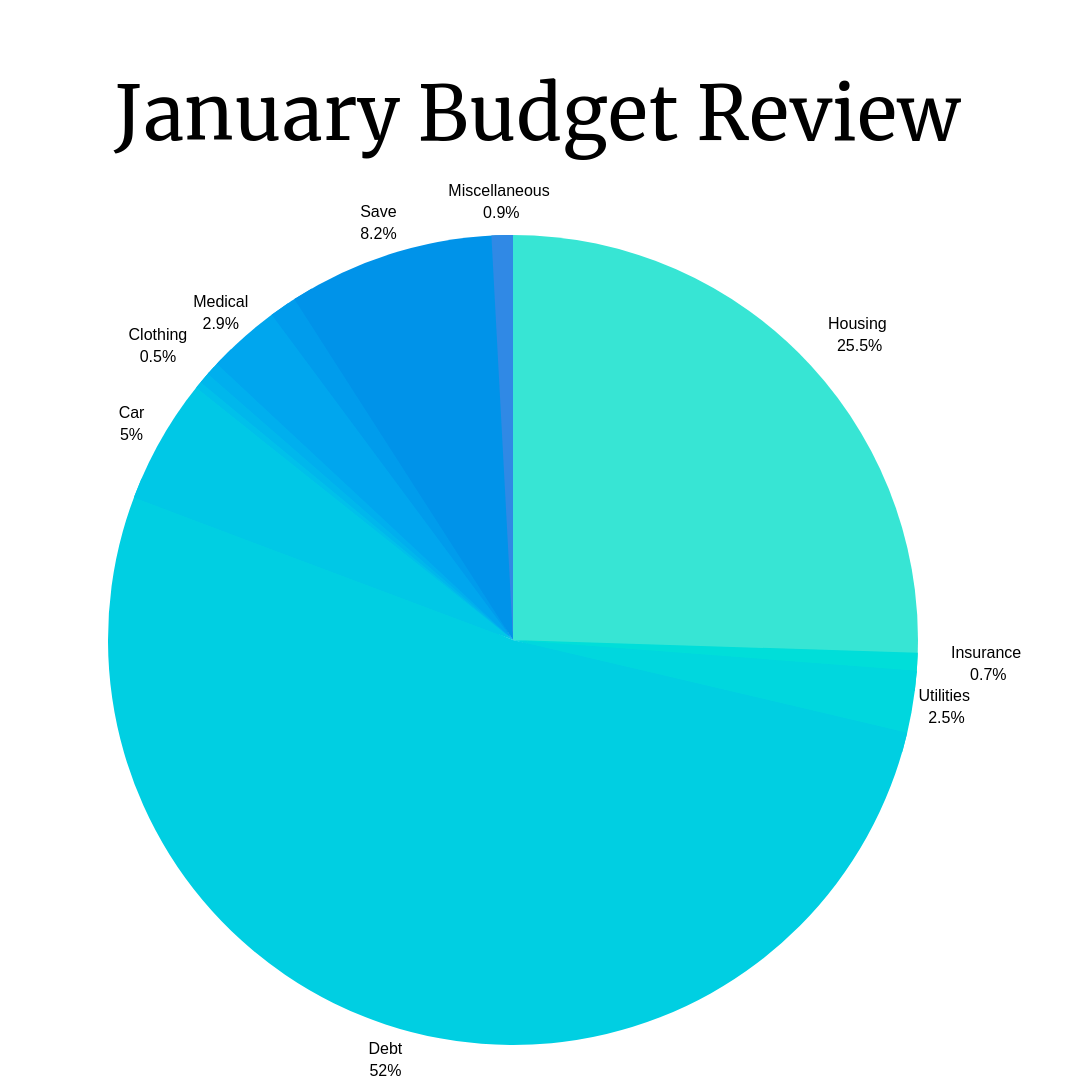

Spending Breakdown By Category and Percent

Here’s a breakdown by category and percent of my total monthly spending. I love that the biggest category is debt payments! This means that I’ll be able to free up 50% of my budget when the debt is completely paid!!!!

Sinking Funds

For more information on how I manage my sinking funds, and the 5 sinking funds I think every budget should have, see this post!

This month, we spent a total of $550 on sinking funds, broken down as follows:

Birthdays/Other Gifts - $150. My son gets invited to no fewer than 6,487 birthday parties a year, so this fund really helps when those unexpected gifts need to be purchased. This month, I also used store credit (from returning unwanted Christmas gifts) to purchase a baby shower gift for a co-worker. I love using store gift cards from returning unwanted gifts to fund future gift purchases! Such a money saver!

Christmas - $200. Each payday, I add $100 to a Christmas sinking fund. By the end of the year, I have $2,400 to spend on Christmas!

HOA Dues - $100. I add $50 every payday to an HOA sinking fund, so I can pay the dues without stress or worry when they come due at the end of the year.

Medical/Dental - $100. This month, I put $50/payday into my medical/dental sinking fund. I’m going to have to start beefing this category up, because we are expecting at least $200/month in doctor visits and prescriptions for the next several months, for a course of treatment our doctor has recommended. It’s fine. Everything’s fine.

Debt Payments

In addition to my standard monthly payment of $375.63, I make an additional payment to my student loan (my only non-mortgage debt) on each payday. My extra payments this month totaled $3,237.00.

Here, I break down those 2 extra payments, so you can see exactly how it’s done!

NOTE: When I budget, I usually round up, instead of budgeting the specific bill amount. Anything left over, I throw at the debt.

Extra Payment - January 1, 2019 = $1,762.00

For this extra payment, $1,132 came from the January 1 paycheck. (See my exact budget for this paycheck on Instagram, in my saved stories). But, where did the rest of the money come from?

$500 came from hubby’s pay

$1.68 came from my life insurance payment leftover (I budgeted $50, but the actual amount is only $48.32)

$50 was leftover from our New Year’s Eve budget that we didn’t spend

$77.36 came from my “extra debt payment” envelope. Whenever I have extra money leftover in any category, I add it to this envelope between paydays. When the next payday rolls around, I add whatever’s in this envelope to my debt payoff!

$0.96 from my cushion/buffer envelope to bring the total to an even $1,762!

Extra Payment - January 15, 2019 = $1,475.00.

For this extra payment, $803.33 came from my January 15 paycheck. But, where did the rest of this money come from?!

$0.82 left over in the grocery budget

$4.37 left over from my student loan payment (I rounded up when I budgeted)

$114.33 from my side hustle payday

$40 from returning unwanted gifts

$175 from HOA (the bill was $175 less than we budgeted for)

$84.79 left over in my buffer/cushion envelope from the prior payday

$250 donated from hubs’ pay

$2.36 out of my buffer category from this paycheck, to bring the total to an even $1,475!

Total Debt Update

I began my debt free journey in January 2017 with $104,901 in student loan debt. I started this January (2019) with a student loan balance of $48,301. As of January 31, 2019, the balance is $44,907. With this month’s debt payments, I am officially at 57% PAID!! Whoop!!

And that’s a wrap! How about you?

How did your budget and/or debt repayment go in January?

Are you making progress on your 2019 financial goals?

Do you have any questions about budgeting? Leave them in the comments below!

Don’t forget to pin this article so your friends can see, too! Just click the image below!