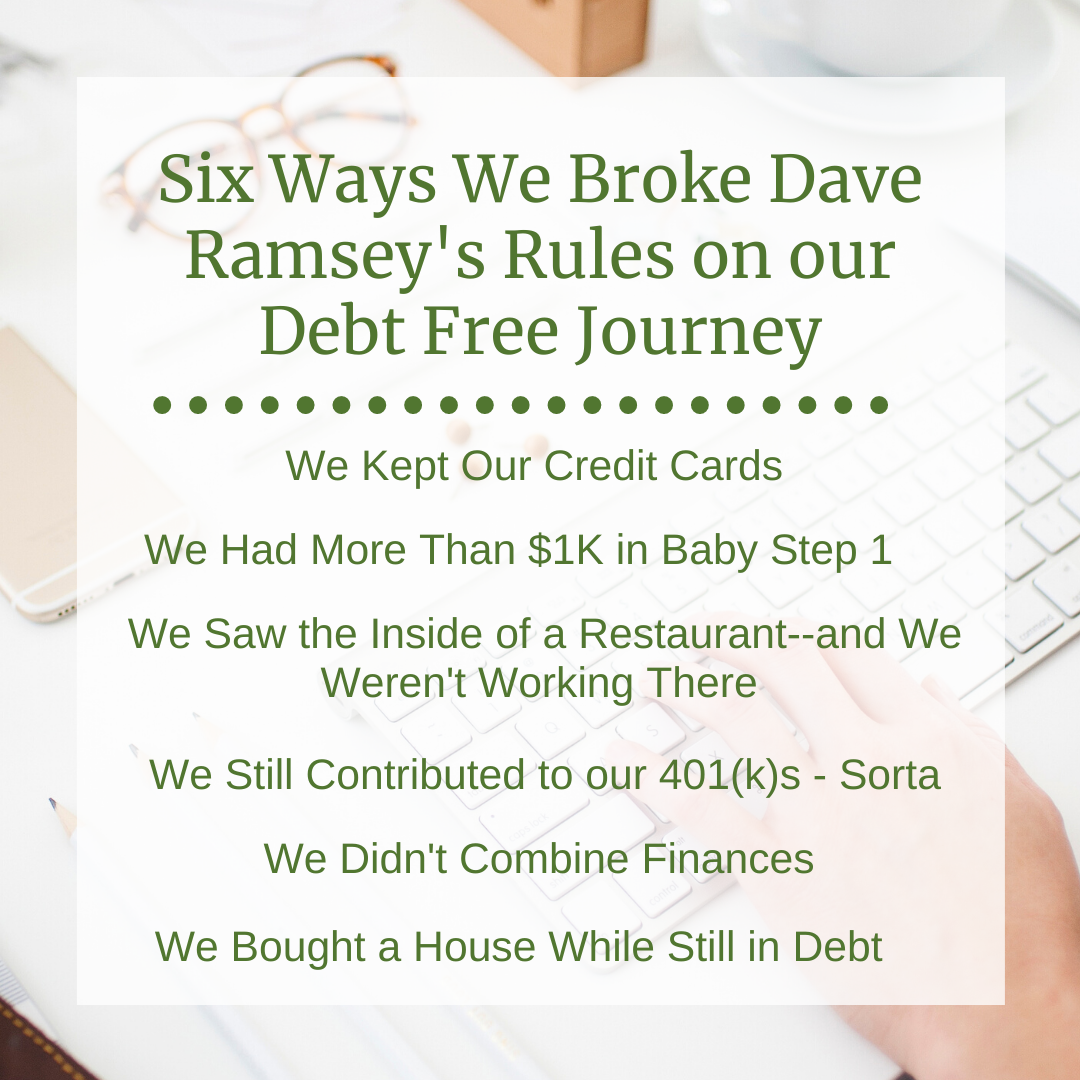

Six Ways Our Debt Free Journey Broke Dave Ramsey's Rules

If you’ve been around the personal finance community for long, chances are you’ve heard of Dave Ramsey and his 7 Baby Steps to Financial Freedom. I always say that these are the principles we used to help us pay off all of our non-mortgage debt ($105K of debt in all) in less than 3 years. But in reality, once I start examining it, the truth is, we really didn’t follow Dave’s plan all too closely. In fact, we deviated from it significantly in many respects.

And you know what? It’s totally okay. The plan we used still worked and still led us to debt freedom.

When devising a debt pay off plan or personal finance plan for yourself, you have to remember that personal finance is personal. I encourage you to find a sweet spot that works for you: something that challenges you to hit your goals—but isn’t so challenging that you simply give up altogether.

Here are the ways we deviated from Dave’s plan and how our journey may look different from yours. And spoiler alert: we still became debt free even with these deviations!

RELATED: How Our Debt Free Journey Began

We Kept Our Credit Cards

Now, I haven’t had a credit card since I was 18, but my husband has always had one and couldn’t be convinced to give it up on this debt free journey. We never carried a balance on his card after paying it off years ago, but he still wanted to keep it around. You know, just in case. He knows a credit card is not an emergency fund, but old habits die hard. So we kept the card, but we didn’t carry a balance on it.

What’s more, I applied for a credit card for the first time since I was 18 in the middle of my debt free journey. Whaaaaaaaat? Yep, I did. I wanted to try my hand at using credit card points & miles to travel for basically free, which I’ll talk more about in an upcoming post. When we went to NYC to celebrate becoming debt free, we used points our flights, and only paid $11 total for 2 round trip flights. Yes, please!!!).

We Had More Than $1K in Baby Step 1

As the saver in the family, I have always kept more than $1K in my savings account. In fact, I practically start to break out in hives if it dips below $10K. Part of the reason Dave recommends taking your savings down so low is so that you will feel the pressure to complete your debt free journey as fast as humanly possible. But I was never comfortable virtually eliminating my savings and putting my family at risk, particularly since we knew our journey would take almost 3 years. A lot can happen in that time, and we wanted to be prepared for the unexpected.

We Saw the Inside of a Restaurant and We Weren’t Working There

Dave is famous for quipping that you shouldn’t see the inside of a restaurant while on your debt free journey unless you’re working there. We didn’t go three entire years without eating out and that probably comes as no surprise to you. If you can go 3 years without eating out, you have more will power than I ever will! We did, however, reduce our eating out budget, even though we seemed to regularly blow it. Eating out was our biggest weakness on our debt free journey—and if you have that weakness too, hey, you aren’t alone.

We Contributed to Our 401(k)s—Sorta

My husband and I both work for the same firm. Our firm contributes 3% of our salaries to our 401(k)s as a gift every year—whether we contribute or not. So while we technically weren’t adding extra contributions to the 401(k) during this time, we were contributing something, even if it was in the form of a gift, and was only 3%.

We Didn’t Combine Finances

Dave would definitely frown on this one. He argues that you have to combine finances and work together as a team to make any financial progress. My husband and I earn approximately equal salaries, but he’s a spender and I’m a saver. Even though we’ve been married for 8 years now, I still hate the idea of combining finances. I like knowing that there is only one person spending from my account—which makes it easy to manage at all times.

So, we keep our accounts separate and we split the bills. But we do have the same financial goals and agreed that we should work hard to become debt free and advance our way through the baby steps. That similar mindset has definitely helped us achieve our financial goals together—even if our accounts are separate.

If you think becoming debt free isn’t possible because your spouse refuses to combine finances, I’m here to tell you otherwise.

We Bought a House While in Debt

Dave suggests not buying a home until you are completely debt free, have saved up 3-6 months of living expenses, and have saved up at least a 20% down payment. Your down payment is baby step 3(b) in the baby steps.

We didn’t do that.

In fact, we bought a house—like most people do—while we were in the throes of debt, long before I began taking any of this Dave Ramsey stuff seriously. Looking back on it, I don’t regret buying when we did. And we’ve been fortunate and blessed that we didn’t have any catastrophes while paying off debt (i.e., roof replacement, broken A/C unit, etc.).

Your Turn!

Have you deviated from Dave Ramsey’s steps? Tell me how in the comments below!

If you’re interested in finding out the strategies we did use to help pay off 6 figures of student loan debt, sign up below for my Free Guide!